For high-quality lending decisions, financial institutions carry out an all-round analysis of a client's business. They examine formal reporting and managerial data, business scheme and model, cross-check and analyze obtained information. At the same time, you can see that specialists involved in data collection and processing of information, and decision-making on loans cannot always quickly focus on the main aspects and specifics of a particular field of activity. Understanding the specifics of each individual field/line of business allows you to conduct the first client meeting more effectively and competently, in the course of which you can determine the potential client’s needs taking into account the type of business, assess the prospects of cooperation with the client, and prepare him/her for the more detailed business analysis, and, more importantly, to conduct a meaningful and high-quality business analysis, which involves:

Asking the business owner and other persons involved in the business competent, correct and pertinent questions, processing obtained information, cross-checking it, analyzing it allows you to make high-quality loan decisions and decisions on further cooperation with a potential client.

This article focuses on the analysis approach used for the following types of business activity:

Before delving into the topic, we would like to note that during the first stage of analysis it is important to understand what kind of business the client is engaged in, study the business scheme and model. This helps you to define your course of action when analyzing any field of activity. In addition, clients from each sector will usually also have individual specifics. Therefore, invite the client to talk about how the business is organized, how information is stored, how calculations are done before examining available formal and managerial documentation.. This will help make the analysis more sensitive and focused.

In this article, we will look at the main aspects and nuances to focus on when analyzing businesses of the above-named industries.

Let us start with trade.

| TRADE |

Retail and wholesale trading companies purchase goods from other companies (including manufacturers) for then reselling them. Examples of trading activities may include trade in groceries, household goods, clothes, footwear, stationery or flowers etc. The points of sale can be physical outlets and online stores (virtual). The goal of any trading business is to resell goods for a price higher than the purchase price. In other words, the sales price should be high enough to cover the purchase price, operating costs, and leave enough profit for the business ‘to make sense’.. Thus, in a general sense, earnings in trade are formed as the difference between sales and purchase prices, and the business itself focuses on buy & sell transactions.

Retail and wholesale trading companies purchase goods from other companies (including manufacturers) for then reselling them. Examples of trading activities may include trade in groceries, household goods, clothes, footwear, stationery or flowers etc. The points of sale can be physical outlets and online stores (virtual). The goal of any trading business is to resell goods for a price higher than the purchase price. In other words, the sales price should be high enough to cover the purchase price, operating costs, and leave enough profit for the business ‘to make sense’.. Thus, in a general sense, earnings in trade are formed as the difference between sales and purchase prices, and the business itself focuses on buy & sell transactions.

The analysis will focus on issues related to thepurchase and sale of goods, as well as on operating costs. It is important to analyze the following information:

- whether the trading terms meet current client requirements and market trends;

- seasonality;

- marketing policy and promotion of goods on the market;

- balance sheet indicators of a trading enterprise, including inventory turnover rates;

- profitability trends and change-factors;

- sale/purchase schemes; contractual relations with suppliers and buyers: study contracts, the terms of delivery of goods, analyze the customer base, as well as the terms of sale of goods, find out if payment deferrals are possible etc.

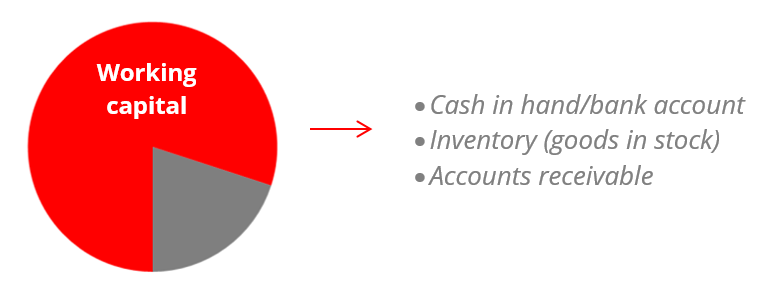

The balance sheet profile of a trading company is usually characterized by a high share of current assets: cash, inventory, and possibly accounts receivable (especially relevant in the case of wholesale) (see Chart 1). To conduct continuous trading activities, businesses need cash and cash equivalents. However, the structure of current assets may differ from company to company, depending on the specifics of a particular client (business). Retail chains normally sell goods without payment deferrals (retail customers usually pay for goods immediately upon purchase), therefore the share of accounts receivable from customers in their asset structure will be low. In wholesale trade, the situation can be different: the share of accounts receivable from customers for goods can be high. Many wholesalers offer deferred settlement terms as part of their terms and conditions of cooperation.

Chart 1. The share of current assets (working capital) in the asset structure

However, if, for example, a business has invested in the purchase of premises, then the structure will be different with a high share of fixed assets and/or their predominance over working capital.

Inventory is the most important asset for a trading company. During the analysis, it is worth paying special attention to the structure of inventories and turnover rate which measures how fast goods in stock turn over (sell) on average. With regard to the structure of goods, a financier should determine which goods are liquid and which goods may be subject to write-off or will be sold at a large discount; which of the goods belong to the business, and whether there are goods on credit or on “sell or return” terms, what are the entrepreneur’s liabilities on purchased goods well as what the mark-ups on different groups of goods sold are and what the weighted average mark-up is at each point of sales.

It is important to assess whether the volume of current inventories is compatible with the volume required. In this way, you can identify the risk of "overstocking" or "understocking" goods.

Compare the client’s inventory turnover rates with those of similar businesses and average industry indicators. If your client’s inventory turnover rate is higher or lower if compared to similar businesses and industry-/region-average indicators, then this is a reason for a more careful examination of such deviations. For example, if the average inventory turnover rate for similar trading businesses in a given region is 5 days, then a ratio of 8 days for your client may be a reason for more detailed investigation of reasons. Of course, for different commodity groups, inventory turnover rates will differ: perishable goods should turn over faster than clothes or equipment.

It makes sense to discuss any discrepancies with the client. A very large, non-typical volume of goods in stock may have its objective explanation. For example, a client changed his/her business line and purchased a new group of goods, which may be dictated by demand. In order to make the offer more attractive and meet customer demand, the client needs to offer a certain assortment. In this case, at a particular point in time, the client may have an unusually large volume of inventory if compared to previous periods or similar clients. But there may be another situation where a large volume of inventory can be attributed to lower seasonal sales than expected so that our potential client may be forced to sell these at a discount. It may also turn out that the good is not in demand at all. Generally, a large amount of unclaimed inventory may indicate that the potential client has a poor idea of the level of supply and demand in the market. There may also be other factors: for example, the late arrival of a certain batch of goods delivered much later than expected due to closed borders etc.

But it is not indicated to label high or low inventory turnover rates as good or bad. It is important to look at the actual situation of client and evaluate it on a case-by-case basis.

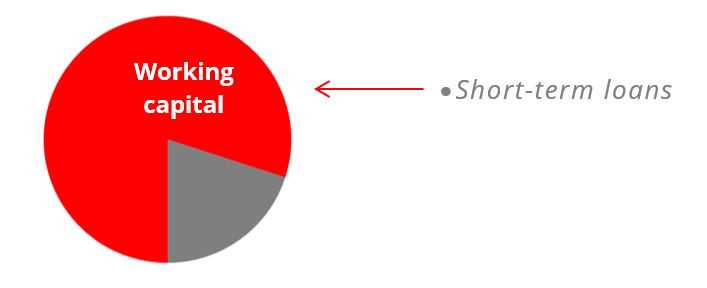

On the balance sheet of a trading company, we can see short-term liabilities comparable to its working capital (see Chart 2). If there is a bias then it makes sense to examine the situation more closely, e.g. if inventories are financed with "long money" or there are "short-term liabilities" that are not comparable to working capital assets.

Chart 2. The purpose of short-term loans is to finance working capital

It is also important to analyze the quality of accounts receivable from customers. If an analyst understands that the debt of a customer is unrecoverable, then this debt should not be included it in the balance sheet as accounts receivable. This may also affect future inventory purchases.

Trading businesses are subject to demand fluctuations: demand can be high or low, depending on the commodity group and season. There are many options to measure profitability of sales (ROS, i.e. return on sales reflects the share of profit in total sales). For example, for a retail store, you can use the classic approach: the ratio of net profit to total sales revenue. The return on sales ratio shows you how much profit is earned per one monetary unit of revenue. This indicator must be higher than zero. Sometimes, in order to attract more customers or “push out a competitor,” owners (managers) decide to reduce trade mark-ups, which can ultimately reduce their profit margin. It is worth understanding these nuances and being able to assess the profitability of sales as this can be indicative of pricing policy issues.

As with other types of business, it is also important to assess quality indicators of trading companies, such as quality of management, staff turnover rates, marketing, quality of services, quality of the documentary flow regarding various authorities (tax authorities, landlords, etc.). Let's take personnel as example: it is common knowledge that one seller is able to sell a certain good, while another seller cannot. Sometimes there is a direct relationship between the level of sales and staff turnover. And the staff turnover may increase or decrease sales volumes at an outlet. The marketing policy also affects the level of sales in a market, while poor quality documentary operations can undermine the smooth running of any business.

While operating conditions of different trading companies may vary significantly, there are a few common factors that indicate a ‘good’ state of affairs and make trading businesses more attractive to financiers:

- favorable location;

- modern approach to customer service;

- high demand for goods;

- ever-growing customer base and the presence of regular customers;

- well-established and stable cooperation with suppliers;

- stable liquidity;

- sufficient and high-quality inventory and a sufficient range of goods;

- permanent staff and low staff turnover;

- positive profitability; retained earnings sufficient for business development.

| PRODUCTION |

Manufacturing is a field of activity where raw materials are processed and converted into ready-for-sale goods (either semi-finished and/or finished goods). For this field of activity, technologies, equipment, specialists, distribution channels, etc. are important. Production can involve the use of high-tech equipment and manual labor.

The starting point of the analysis of a manufacturing business is the study of what is produced, the business scheme and the production cycle. It is recommended to get answers to the following questions:

- What does the business produce?

- Is there demand for the product or not?

- Is the technology used up to date?

- What is the quality and price of the goods produced?

- Is there competition? How competitive is our client in terms of product quality, price, etc.?

- How is the production process organized?

- What equipment is involved in the production cycle?

- What is the maximum and actual equipment capacity? What equipment is involved in the production cycle? Is it used at its maximum capacity or only partially?

- Is there a seasonal dependence of production?

- What is the duration of the production cycle?

- What are the volumes of production and the volumes of sales?

- Other

Depending on the scale of the enterprise and the production process, the approaches to collecting and processing information will also differ. If it is a small production business (for example, one production line for chips), then the business process will be quite simple and easy to analyze. But if an enterprise produces many different products or there is one production line that produces different types of products, then analyzing the production cycle will be quite laborious. In this case, it is recommended to divide the core production process and auxiliary production and analyze processes separately by area of production (by production line, by workshop, etc.).

In any case, it is important to assess production volumes and distribution of products. These are two interdependent indicators. For a business to work effectively and develop, it is important to produce such goods and in such amounts that can be realistically sold. If a manufacturer produces more products or fewer products than the business can sell, this is usually bad. In the first case, this will mean accumulation of unsold products in warehouses and lost income. In the second case (when a manufacturer produces less than it can sell), it may indicate inefficient organization of production, lost opportunities and/or problems in production as well as the risk of losing customers.

Estimate the demand for products and compare the volumes of goods produced and sold. After all, the volume of production depends on the demand for products in the market. These are two inter-related indicators. Analyze trends in the volumes of production and sales, look at the seasonality and consider the ups and downs in the production of a particular product. It should be kept in mind that manufactured products that could not be sold within reasonable time limits will usually be written off in the future. Analysts often make the mistake of using production volumes to assess the volume of sales.

One serious aspect to be considered is the fulfillment of contractual obligations by the client under supply contracts. Therefore, it is important to study the client’s supply contracts with customers. Failure to fulfill delivery plans under contracts may result in a decrease in revenue, profits and penalties envisaged by supply contracts. Let us take flour production as an example: A company produces 1,000 tons of flour per month on average. However, according to supply contracts, over the past 6 months, it has been selling only 500-600 tons of flour per month. This means that the rest of the manufactured flour has been going on stock. How long can flour be stored in a warehouse and will it be sold in the future at the same price …? This is a cause for careful analysis.

Production implies that an enterprise must have working capital needed for manufacturing goods. When analyzing production enterprises, it is important to pay attention to the efficiency of the use of current assets. It is recommended to pay special attention to the stock of raw materials available for the production cycle, evaluate and compare the following information: storage periods of raw materials and their turnover, purchase amounts and the sufficiency of raw materials as per calculation to ensure a continuous production process. It may turn out that material is being stocked that will not be used (overstocking). It is worth examining this situation in more detail and finding out why this happened.

In the process of the analysis, we pay attention to the condition of equipment, its service life, the source of financing its procurement, availability of ownership and other documents (certificates etc.) and whether such equipment is liquid today (easy to sell). We should understand that production activities are associated with high production risks. Firstly, if equipment is used without required documents, there may be a risk of fines and penalties imposed by respective supervisory authorities (due to violations of fire safety, labor protection requirements etc.), and you will not be able to take such equipment as collateral if the client does not have ownership documents for it. In addition, equipment that is used without proper documentation and/or without proper care can have a negative impact on the environment and personnel.

Fixed assets are usually characterized by a rather long service life, but you should keep in mind that they are subject to regular maintenance and overhaul, which implies costs.

It should be noted that the organization of production usually requires large investments, therefore we need to look very carefully at the sources of funding, i.e. own investments or borrowed funds.

Remember that production activities typically require more permits and licenses than trade and services. If any permits/licenses are missing, this implies increased risk. Unlike service and trading companies, manufacturing companies are less flexible in the event of emergencies and force majeure situations. Therefore, it is best to be skeptical and assume that such events can occur in any manufacturing process. The business cycle is usually longer and, therefore, liquidity may vary at certain points in time. Manufacturing relies on qualified personnel who operate and maintain production facilities.

In a trading business, the issue of pricing and cost of goods sold is quite clear. As opposed to this, in a manufacturing business, calculation and accounting of production costs depends on the accounting methodology adopted by the company for cost accounting and for calculation of the cost of production.

It is important to understand the manufacturer's own calculations. This can save you a lot of time: once you understand how to calculate certain positions, you also understand what and how you should calculate. You study how production costs are calculated by the business and what costs are included in the cost calculation per unit of production. This calculation may include the cost of raw materials and supplies, wages and other remuneration of personnel directly involved in production, payroll tax deductions of these workers, utility costs and the cost of heat and energy resources consumed in the production process, the cost of waste/losses and other production costs etc.

We have listed only the main features of the analysis of a production enterprise and what to focus on when collecting information about production, but even from this, it is clear that the analysis itself and the approach to it can be quite difficult. Often, it may take up to several days for a loan officer to collect and process all necessary information, and involvement of different specialists on the side of the manufacturing company (specialists from the production hall, accountants, managers etc.). Therefore, loan officers must have a high level of training.

| SERVICES |

Cafes, restaurants, hairdressers, beauty salons, car washes, private kindergartens, fitness clubs, foreign language schools, legal services etc. are examples of service providers. This spere of business typically has the common advantages such as minimal start-up investments and high profitability levels. Of course, there are service areas where start-up investments caan be significant, for example, IT or car services.

Cafes, restaurants, hairdressers, beauty salons, car washes, private kindergartens, fitness clubs, foreign language schools, legal services etc. are examples of service providers. This spere of business typically has the common advantages such as minimal start-up investments and high profitability levels. Of course, there are service areas where start-up investments caan be significant, for example, IT or car services.

Companies providing services have individual specific features which may differ significantly depending on business specifics. These will affect profitability and balance sheet features, and, ultimately, the focus of the analysis. For example, in the case of taxi services, the analysis will usually show a large share of fixed assets on the balance sheet total, while the share of fixed assets is likely to be low in the case of legal services,, and, therefore, the focus of the analysis in the first and second cases will be different. From the table below, you can see that for all types of services, the analysis will focus on the availability of intellectual/skills resources (i.e. competent specialists), working scheme and the number of orders, while the need to lookdeeper into working capital and fixed assets will depend on the specific features of a given business.

The length of the business cycle in the services sector may also vary significantly: from several minutes/hours (hairdressing salons, photo studios, cinemas, other consumer service providers) to several months (companies that work on large individual orders).

Consequently, the financial ratios of service providers will vary significantly, especially those based on balance sheet indicators, and deviations from standard normative values can also be significant: for example, working capital turnover rate, the ratio of fixed assets, the debt-to-equity ratio etc.

Table 1. Comparing different types of service providers

|

Activities |

Specialists |

Number of orders |

Operating scheme |

Current assets |

Fixed assets |

|

Car service |

|

|

|

|

|

|

Medical services |

|

|

|

|

|

|

Passenger and cargo transportation |

|

|

|

|

|

|

Rental services (real estate, equipment, vehicles) |

|

|

|

|

|

|

Consulting (legal, financial) |

|

|

|

|

|

|

Information Technology |

|

|

|

|

|

|

Cleaning services |

|

|

|

|

|

|

Tourist services |

|

|

|

|

|

As a rule, the share of current and fixed assets in the structure of the balance sheet will be relatively low in most cases. Inventories in the service sector either do not exist at all (for non-production services), or account for an insignificant share in the structure of current assets (spare parts and components). Accounts receivable may account for the main share of current assets, while for enterprises that work on condition of 100% advance payments by customers, working capital will consist primarily of cash on hand and in bank accounts.

Service sector companies do not usually have long-term liabilities on their balance sheets. But there may be exceptions, as in the case of services involving the operation of fixed assets. Short-term liabilities consist of accounts payable to suppliers and advance payments received from customers and other payables, and, in the case of larger organizations, these are mainly accounts payable to subcontractors. Consequently, service enterprises tend to have small amounts of passive accounts.

In most cases, the cost of services will not be calculated, since no raw materials are involved:

- For services based on the operation of fixed assets, the main expense is associated with their maintenance.

- For knowledge- and information-based services, the main expense is labor costs.

When analyzing service companies and depending on the specifics of each client, the focus should be on the business scheme, the number of standing orders, staffing, quality of services and/or collection of information on the expenditure side.

The specificity of the services sector and its diversity make it rather difficult to analyze the activities of such enterprises. And for this reason, loan officers must learn to focus on common/standard features and the specific features of each individual area of activity of the services sector.

In conclusion, all three areas of business activities - trade, services and production - require a different approach to the analysis. More than that, not only a different approach but also special knowledge. Trade is usually easier to analyze than services and manufacturing. In addition to the nuances that we highlighted in this article, there are other specific features that exist in each separate industry. And the task of all specialists engaged in the analysis of any sphere of business is to be attentive to these features, since an error in calculations can lead to an incorrect result and decision.

It is not uncommon to start searching for suitable candidates by publishing a job advertisement. At the same time, many job requirements are often worded in a vague manner or limited to general phrases like "working experience is welcome."

This article focuses on an important aspect which is often overlooked by financial institutions, i.e. how to make your recruitment process efficient. After all, this process requires preparation and begins long before posting the advertisement for a vacancy.

Generally speaking, we can specify a few key conditions for ensuring high-quality work with personnel:

- A systematic staff search and selection process;

- A well-designed internship program;

- A system of regular staff evaluation of achievements and competencies;

- A system of training needs assessment and regular training;

- Conditions for career advancement and career planning.

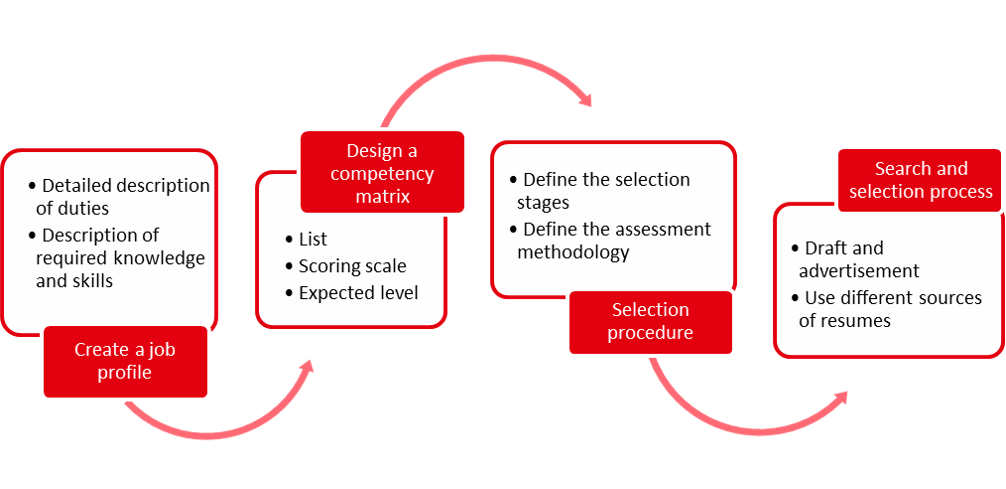

This article provides a detailed description of the first stage of staff development activities: best practices in organizing staff search and selection process, including a description of mandatory components and practical recommendations on their successful implementation.

Importance of the preparatory stage

The importance of quality staff recruitment is difficult to overestimate. Hiring a candidate who cannot cope with assigned tasks due to a lack of necessary qualities and skills leads to significant losses of time and resources of an organization, as well as to lost opportunities.

To find the right employee, it is important to start with preparatory activities, not only focusing on formal requirements but on analyzing which candidate would be able to perform the tasks associated with a certain position. It is also necessary to create conditions for objective and prompt decision-making by elaborating clear selection stages and evaluation criteria for candidates.

It is important for the HR department of any institution to carry out preparatory work that will ensure the most effective process of finding suitable candidates and, most importantly, create conditions for hiring candidates who are most suitable for a concrete position.

As a result, due to targeted staff selection, a decrease in training costs may be expected, higher staff efficiency and lower staff turnover.

As in the case of any other process, for successful implementation of the staff selection process, it should be systematized and described in detail. This will lay the foundation for objective assessment and selection of the most suitable candidates for the specific task.

How should this process be organized according to global best practices?

Designing a job description/profile

As the first preparatory step in quality recruitment, it is recommended to develop a detailed job description for each existing position at a financial institution.

It is important to indicate the desired education or work experience as well as necessary, specific practical knowledge, skills, and qualities that a successful employee should have for a specific position.

A job profile for each position is prepared as a separate document which should include the following information:

- List of responsibilities in a specific position;

- Requirements to potential candidates;

- Proposed working conditions.

A table below outlines a sample structure of a job profile description.

|

Sample Job Description: Structure |

| (1) Purpose / role of the job |

| (2) Sphere of the main responsibilities |

| (3) Round of duties |

| a. Primary (core) duties |

| b. Secondary duties |

| (4) Requirements to the candidate: |

| a. Education / Working experience |

| b. Professional knowledge |

| c. Competencies (skilss, abilities, personal qualities) |

| (5) Working conditions and employee rights |

| a. Remunaration structure |

| b. Working time and vacation |

| c. Professional development plan |

| d. Evaluation of efficiency |

| e. Career advancement opportunities |

It is important to define clearly the primary and secondary duties for each position. For initial compilation of this list, it is useful to set up a working group including specialists of the HR department and the department to which this job belongs. You can start by defining the general tasks of the department and then indicate the functional duties of each employee of this department.

The more precise this list is, the easier it will be to find the right candidate for a concrete position. With a clear idea of what duties will be performed by an employee in a concrete position, it will be easier to proceed.

The next step is to determine the knowledge, skills, and personal qualities that an ideal candidate for this position should have. It is important to pay special attention to this item.

In the "Requirements to the candidate" item, employers often indicate formal requirements, such as higher education, computer skills. However, it is more efficient to select candidates by their personal qualities and professional skills. And there is a good reason for this.

- For example, even if a potential candidate for the arrears department is suitable in terms of education and comes with excellent recommendations but is not good at dealing with conflict situations, then s/he is not likely to cope with his/her duties in this job.

| Here are some of the skills that candidates must have to work at a financial institution |

|---|

|

It is easier to describe required skills by analyzing the list of daily tasks and match them with various competencies that are easily available in the public domain. As a next step, you should choose the most important skills for carrying out the daily tasks associated with a given position. You should also remember about secondary duties and add the respective skills to the list.

Another useful method of collecting the necessary competencies is to analyze the qualities of successful employees in this position in your organization.

Determining the required competencies is not an easy task, but by doing this you can significantly improve recruitment efficiency. Once you have completed the description of duties and requirements to potential candidates, you have the necessary basis for the next step.

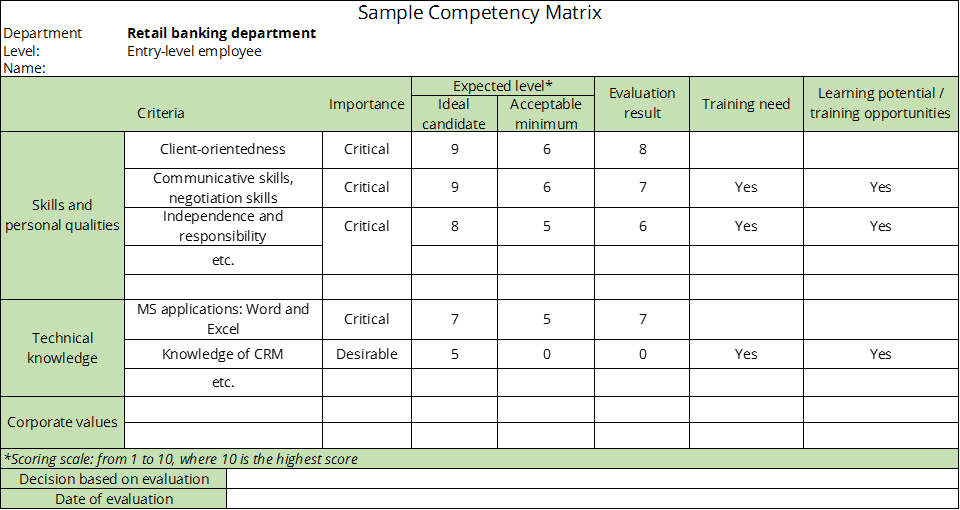

Drafting a competency matrix

In this matrix you list all competencies required to perform the duties in a particular position. It is recommended to derive competencies from the competency list compiled for a given job profile and add them to the matrix, usually grouping them in personal qualities and technical skills. It is recommended to limit the list to the most indispensable competencies for each position. If the list is too long (more than 10 competencies), this will complicate assessment. Given that different positions are associated with different responsibilities and responsibility levels, the number of competencies on the lists for different positions may be different, depending on the complexity of each concrete position.

The next step is to define a measurement scale, for example, a scoring scale from 1 to 10 (where 10 is the highest score), or a scale of qualitative indicators: "Low - Medium - Above average - High", and, accordingly, indicate the proficiency level required for each skill for successful performance in a given position.

As a rule, a competency matrix is developed for a specific department and for each staff level: a specialist, a senior specialist and the department head. Accordingly, the expected level of proficiency for a particular skill will be indicated depending on the expected level of experience required for each position.

When defining the scale of expectations of an ideal employee, it is important to consider the degree of importance of each competency for the respective department.

- For example, employees of the Retail Department must have a high level of communication skills (9-10 of 10, based on the scoring scale mentioned above). As for candidates for positions in the Accounting Department, while communication skills are important for intra-team interaction, such candidates are not expected to have the highest level of communication skills.

At each of the stages described, it is important to avoid generalization. It is recommended that in your description, you indicate specific skills required by your institution.

For example, when it comes to credit risk specialists, they are expected to have a high level of analytical skills. This requirement can be specified as follows:

- Analytical skills: ability to process quickly large volumes of diverse information, identify the most important aspects, possible risks, draw independent conclusions and propose solutions.

Or, another sample description of communication skills expected from a loan officer:

- Communication skills: ease in communication with potential clients, ability to explain products/procedures correctly and in an understandable way, ability to collect effectively exhaustive information for credit and risk analysis, ability to handle objections, resolve conflict situations.

It is important to add management skills to descriptions of leadership positions. For example: initiative, planning skills (organizational or control skills), the ability to develop and motivate others. The presence of required management skills should be envisaged as a prerequisite for career advancement. In such cases, the development of these competencies will serve as an incentive for experienced employees with a prospect for promotion.

As an additional option, competences can be divided into critical (indispensable) and desirable. The first category includes qualities or skills that are absolutely necessary and without which high-quality performance of the functions described for a given position will be impossible or extremely difficult.

- An example of critical competencies: attention to detail for the position of an Accountant

It should be borne in mind that a competency matrix describes an ideal employee for a given position, and potential candidates may not necessarily have all the necessary qualities at the desired level. In this case, it is important to pay attention to the potential of candidates for developing a particular skill and available resources in your organization (for supporting candidates in developing needed skills). It is also recommended to pay attention to the readiness of candidates for further growth and their additional strengths that may (partially) compensate for the insufficient level of any of the required skills.

At the same time, if no candidate is found who meets the minimum set of critical competencies, it is recommended to avoid compromises and continue to search, because hiring an unsuitable candidate will usually have more negative consequences and will cost your institution more in terms of time and money than continuing to search for a more suitable candidate.

It should be remembered that not everyone is suited for any job, even if a lot of time and effort is invested in training. In most cases, employees who cannot cope with tasks due to a lack of necessary qualities become dissatisfied and unmotivated, which ultimately leads to unsatisfactory results and staff turnover.

There is a general recommendation for all financial institutions to start with a simple matrix. Over time, this matrix can be adjusted based on staff performance, staff evaluation and experience gained.

Once the competency matrix is ready, it makes an excellent basis for assessing potential candidates as well as evaluate current employees and identify areas for improvement. If staff evaluation shows that some employees lack necessary competencies, identified gaps serve as basis for developing an effective training plan.

There are many options for building such a matrix, and it is important to define a workable model for your institution. As an example, below is one of the possible structures.

Defining recruitment stages and an approach to candidate assessment

Based on the requirements for specific positions, it is worth considering the most optimal recruitment/selection stages for each position. It is important to describe the recruitment process, which includes clear steps, a system of evaluation and a passing score.

Possible recruitment stages include initial screening of CVs, selection of applicants who meet the criteria; general testing, filling out questionnaires; analyzing the results and selecting candidates for an interview; several stages of individual and/or group interviews; conducting specialized testing.

Each of these steps helps to identify different qualities of a potential candidate. By combining different stages with clearly described evaluation criteria, we significantly increase the efficiency and objectivity of the screening process.

It is worth determining selected stages to be applied to in-house candidates. It is also necessary to consider the job level and the selection periods. However, it is important to apply a competency matrix or a list of required competencies for experienced external candidates as well as for in-house candidates. Several years of work in a similar position do not guarantee the expected level of competence.

For interviews, you should prepare blocks of questions to determine the level of certain skills and experience. Accordingly, for an interview, blocks of questions are chosen depending on the required skills determined in the matrix or in the list of competencies required for a specific job. It is also recommended to include situational questions on the previous experience of an applicant.

Here is a possible list of questions to assess self-organization and time management:

- How does your day usually go? Do you plan it in advance?

- How do you prioritize your tasks for the day?

- What helps you with your planning of the day?

- What will you do if you need to fulfill several tasks at the same time?

- Tell us about your plans for the next month.

For convenience and systematization, it is helpful to develop a Candidate Evaluation Form for individual interviews. This can be easily done based on the matrix or list of required competencies.

Questionnaires are a good tool to identify competencies. Group interviews are especially useful for identifying personality types. To conduct them, it is also necessary to prepare questions for discussion and an assessment form in advance. It is also possible to include situational case studies and divide applicants into teams. For an interview, it is advisable to involve several employees since you will need a discussion moderator(s) and an observer(s). For the role of moderators, it is advisable to involve employees of the department for which the applicants are recruited, with support from an HR department specialist in the role of an observer.

It is important to select a proper location for a group interview. On the one hand, participants should feel comfortable to freely express their opinions, so it its preferable to avoid small confined spaces. On the other hand, staff of the financial institution observing the interview process should be able to clearly hear the opinion of each participant.

Depending on the job type, the list of qualities to be assessed will be different and will be selected based on the matrix or the required competencies list. It is important to develop a Candidate Evaluation Form for a group interview.

For example, for a group interview, the following assessment criteria can be included:

- First impression

- Ability to express ideas, communication skills

- Initiative, leadership qualities

- Ability to give arguments

- Ability to work in a team

This screening method is not applicable to all positions and usually used for situations involving many applications for a position. Group interviews are recommended as an efficient method when there are many candidates and competition is high. This method can also be used for evaluating final year students before graduation, in order to select the most talented candidates.

Testing, in turn, can be conducted either to test basic skills / general level of development of applicants, or the level of highly specialized professional knowledge. It is recommended to create an extensive database of possible questions and answer options in advance, to be able to compose different versions of tests without additional input of resources.

It is also important to define the testing procedures in advance, testing time, scoring method and to set the minimum passing score.

It is important to keep the results of initial assessment of selected candidates, in particular, their completed competency matrixes, as this is the starting point of an employee’ further development path.

It is possible to recruit applicants without the expected experience, with only partial technical knowledge, but always with a set of necessary personal qualities. It is recommended to pay close attention to how a candidate fits the job profile, because it is much easier to teach technical knowledge to a person than to change his/her personality.

An in-house professional training system is a good way out. Think in advance of the type of training you can offer to trainees to develop their most important competencies. Depending on the level of the selected candidate, an internship plan is drafted, a teaching method is selected with a list of topics and materials prepared in advance.

Job advertising and searching for candidates

The final stage of the preparation process is the drafting of a job advertisement.

It is important to provide a description of future responsibilities based on the job profile and the main competencies expected. A candidate must clearly understand what functions s/he is to perform.

It is also important to use various media for posting a job advertisement, not just the official website of your organization. Searching for candidates within and outside your organization expands your choice. The wider the outreach of your ad, the more chances that your ideal candidate will notice it. One of the general success factors is to make every effort to ensure that there are enough potential candidates to be able to choose from the best on the market.

It is important to indicate different ways for candidates to submit their resumes and to ensure that none are left without attention or lost in the process. It is recommended to create a positive impression of your organization from the very first contact with applicants by providing all required information and communicate professionally and politely with each applicant.

In conclusion, we present a scheme for organizing the staff selection process based on best practices.

Once you have done this preparatory work and applied the developed criteria in practice, you have a basis for optimizing the process, for a systematic and transparent approach as well as for equal treatment of all evaluated candidates. As a result, the best and most suitable candidates will be selected for long-term work for the benefit of your financial institution. Well selected employees able to fulfill their tasks are the key to higher efficiency, productivity and motivation at lower cost.

The whole world is feeling the impact of the crisis caused by the coronavirus pandemic. Many economic sectors have been hit, resulting in negative economic consequences. Against the background of the pandemic, the Central Asia regional economy is forecast to contract by 1.7 percent in 2020. Experts of the World Bank state that the Central Asian region is experiencing an economic downturn not seen since 1995.[1] According to surveys by national chambers of commerce and business associations, 60% to 80% of companies in most of Central Asia have been severely affected by the coronavirus crisis.[2] Businesses are losing revenue, shops are closing, and supply chains are disrupted.

The crisis is undermining the income and liquidity levels of individuals and legal entities, including micro, small and medium-sized enterprises (MSMEs), as well as their ability to meet obligations to financial (credit) institutions. At the same time, everyone understands that without financial support, businesses will not be able to recover to pre-crisis levels for a long time. But, how can we, under such conditions, build relationships with clients, what and how should we evaluate their situation and outlook, and how can we make lending decisions and/or decisions on changing current loan payments, so that clients can survive the crisis and repay their loans in a way acceptable to financial institutions? In this article, we will give recommendations on what to look for when analyzing businesses during times of crisis.

In general business assessment is aimed at identifying potential trends and negative consequences for business development. At the same time, a high-quality assessment of the financial condition of a business gains more relevance during times of crisis, i.e. in unstable environments. We should keep our finger on the pulse of those enterprises that have already received a loan and now have to service their debt. We should also be able to analyse the businesses of new clients and assess their lending capacity in order to support them and the economy as a whole in overcoming the crisis.

Nowadays, many enterprises and sole proprietors find themselves in a difficult financial situation (temporary insolvency or even bankruptcy), and the task of an analyst is to determine the best support measures for a given client in the current situation. Such support measures could include changing the terms of an outstanding loan or, perhaps, providing additional finance.

During a crisis, business analysis involves objective assessment of a business’ financial condition, plans and development prospects, including its ability to adapt to the current and expected economic situation and trends.

In the process of decision-making about the possibility of cooperation with potential clients and/or support of existing clients, financial institutions take an integrated approach to the analysis (including analysis of market data and macroeconomic indicators, of formal and managerial financial statements, as well as retrospective and prospective business analysis). It is very important to look not only at numbers, but also to understand business processes and the (owner’s, management’s) current and future response to the crisis.

Shops may see declines in sales, manufacturers my see a drop in production output and sales, or the entire production process may come to a standstill because of a lockdown. There is an overall slowdown in profit-making business activities. At the same time, most business costs remain on the same level, and the financial balance in a business is disrupted, which translates into a decrease in financial stability of the business.

In a crisis, some people are prone to panic and to make irrational choices, other people “freeze in denial”, refuse to admit that the situation has changed and continue to live and work as if nothing has happened in the hope that things will resolve themselves on their own. Others, will analyze the situation and look at their business and circumstances as an opportunity for survival, think about possible measures to make the most of the changing environment. They may try to cut costs, find new sources of liquidity and income (for example, switch to a different, more reliable line of business and some may already have a contingency plan in place).

Here are some negative implications for a business that an analyst can observe in the process of analysis:

- decreasing revenues

- decreasing margins of individual business units (sales points, divisions)

- decreasing profits (or even losses)

- reduced liquidity (or lack of liquidity)

- delays in supplies and/or changes in supply chains

- disruption of supply chains

- termination of relations with suppliers

- an increase in accounts payable (to suppliers and creditors). Incurring private debts during such periods can be especially worrisome

- an increase in accounts receivable (customers stop paying on time)

- a decrease in working capital

- lack of finance

- loss of clients

- cancellation (failure) of contract obligations

- etc.

This list is not exhaustive. These negative consequences can even lead to business closure. However, let us look at the problem from a different perspective. In times of crisis, businesses need to be especially flexible, try to adapt to the new conditions, choose the right strategy that could help the business to overcome the crisis. For example, this could mean:

- reducing investment projects

- closing unprofitable production / points of sale

- selling non-core assets

- optimizing costs (especially, fixed costs such as rent, salaries, advertising, transport and other expenses)

- revising the assortment of goods

- entering new markets

- switching to online modes of conducting business

- changing settlement schemes with suppliers and buyers (reduction of payments, barter, etc.)

- making use of all available government support measures and tax opportunities to optimize spending

- etc.

The above-mentioned crisis phenomena and measures to overcome them serve as a hint for financial organizations on what to pay attention to in the process of risk analysis and assessment. However, attention should be focused not so much on the problems as such but on their depth and the tactical and strategic measures taken by the business (owners) to overcome the situation.

In order to find a way out of the crisis, business owners and their teams (depending on the size of the business) explore opportunities, analyse their own business, the market and general economic trends, and they take action. Our task, as analysts, is to recognize measures that are focused on overcoming the impacts of the crisis, to evaluate them and draw conclusions. If a company is "in panic" and does not take any measures, then we must clearly understand that financing it is associated with a high risk. If a business takes active and meaningful actions as a reaction to the current circumstances, looks out for options to adapt to the situation and has a real perspective for the future, then financing such a business is associated with fewer and lower risks. Thus, apart from current financial indicators, the first thing to pay attention to during the analysis is the owners’ (management’s) own reaction, how they assess the situation, how they plan to get out of it, and how this will affect their business productivity and financial performance. A business can still be profitable and have good credit capacity at this time, but the owners’ (management’s) actions/ omissions can lead to a situation where the business may become unable to pay in a matter of weeks or months. Therefore, it is important to see how effective and rational the owners’ plan is, and whether it is focused on business growth and development, even in a difficult period.

What business periods should financial institutions consider and what should they focus on in their analysis?

Analysing past periods. What is the point of this? The purpose of analysing business development over periods preceding the crisis is to understand how much the situation has changed and evaluate the steps taken by the owners. If a business shows a dramatic decline in revenues, profits, has liquidity gaps and/or other negative trends, the probability is high that owners so far have not taken any action or only insufficient action. In this case, it is high-risk for a financial institution to finance/work with such a business, since the owners (management) are likely to continue with their wait-and-see attitude in the hope that the situation will resolve itself on its own.

If you analyse a business that has already survived economic crises in the past, you should look at how they managed this. It is not necessary to delve into accounting records, but sufficient to talk with the owners (management) and find out whether they had to reduce or optimize their business or not, how they got out of the situation back then, and compare this with the current circumstances.

Analysis of the current situation. Get answers to the following questions:

- Can the business cope with the current debt burden? How long will it be able to serve its current debts? From where does the business get the necessary resources? Why is it asking for more finance?

- To what extent is the client now dependent on borrowings?

- Given the current state of affairs, will the client be able to cope with an additional debt burden?

If a business needs a loan only to stay afloat, and you see that it is “frozen in a waiting loop” and/or there are signs of possible negative future trends, then financing such a business will bear high risks. You should always make sure that additional financing will not further aggravate the situation of the business.

Under conditions of uncertainty, the analysis of business prospects should be focused on the current situation and on the client's plans to overcome the crisis. The analysis involves an assessment of the client's plans against the background of general economic trends in the client's market and the economy as a whole, as well as the assessment of the relevance of the client’s plans against these trends (including the likelihood of meeting planned sales targets, income and expenses). If, in the process of your analysis, you see that the client has reconfigured business processes, abandoned ineffective projects, focused on products that are relevant and in demand in the current situation, and has a vision for future business development (at least, for some time horizon), skilfully manages his/her debtors (at least, works with them), tries to maintain acceptable liquidity and own working capital levels, then working with such a client will be less risky.

Therefore, when analysing a business in times of crisis, it is important to assess the business’ tactical, short-term measures, as well as its strategy to keep the situation under control and overcome the crisis. It is also necessary to analyse the core financial indicators (current and expected) which we use to assess business performance under normal conditions. These indicators include:

- balance sheet indicators such as equity, receivables and payables, working capital structure

- trends in the revenue structure, profitability and profit

- business liquidity and safety margin.

Analyse the firm's financial statements and collect managerial accounting data.

Look at the sources of financing that the business uses (owner’s equity, long-term or short-term loans). Having studied the structure of liabilities, you will be able to understand possible causes of financial instability of the business. This could be a high share of debts in the balance sheet total (more than half), which could mean that the business is highly dependent on its creditors.

Pay attention to the speed of growth of accounts receivable and payable, as well as their ratios. Their growth rates should be approximately the same.

Examine financial statements for any losses in the analysed period. You could notice changes in mark-ups, past due loans, receivables and payables.

Assess the liquidity and profitability levels of the business in the short and medium term. In a crisis, it is quite difficult to carry out medium-term cash flow projection and assessment of profit levels. Nevertheless, you can forecast cash flow and profit for the coming months, as well as build positive and negative scenarios (in case of stabilization and/or worsening of the situation). In any case, during situations of crisis and uncertainty, loan officers of financial institutions must conduct regular monitoring of their clients (the frequency of such monitoring is usually higher than in a stable environment). The purpose of monitoring is to check and assess the accuracy of cash flow and profitability forecasts. Monitoring allows loans officers to respond to any changes in the situation in a timely manner and adjust financial forecasts, payment plans and other credit conditions as necessary.

In the current conditions, financial institutions should adjust their conclusions and assessments to the crisis. If you see that a business is flexible and ready to not only manoeuvre with financial resources, but can also skilfully adapt its business processes and schemes, and optimize its activities, thus ensuring financial stability, then you can analyse such a business, evaluate data and take informed decisions with acceptable risk for the financial institution. You may not necessarily encounter super-profits in the process of analysis, but you can evaluate the scale of the changes and measures taken by the business to overcome the crisis and period of uncertainty, and assess the prospects of this business for the future. And this is the basis for finding the best way to support clients in crisis and post-crisis conditions.

[1] World Bank. 2020. “COVID-19 and Human Capital” Europe and Central Asia Economic Update (Fall), accessible by the link https://openknowledge.worldbank.org/handle/10986/34518

According to the estimates of the World Bank experts, with an optimistic outlook, “the economic growth in Central Asia is expected to recover to 3.1 percent in 2021, supported by a modest rise in commodity prices and foreign direct investment. In the downside scenario for 2021, weaker-than-expected external demand, commodity prices, or remittances could dampen the recovery to 1.5 percent.”

[2] OECD Policy Responses to Coronavirus (COVID-19).COVID-19 crisis response in Central Asia, Updated 16 November 2020, https://www.oecd.org/coronavirus/policy-responses/covid-19-crisis-response-in-central-asia-5305f172/

Pictures designed by Freepik